From FNOL to Settlement: Improving Third Party Claims with Data Driven Decisions

Norman Tyrrell

Vice President, Product Management

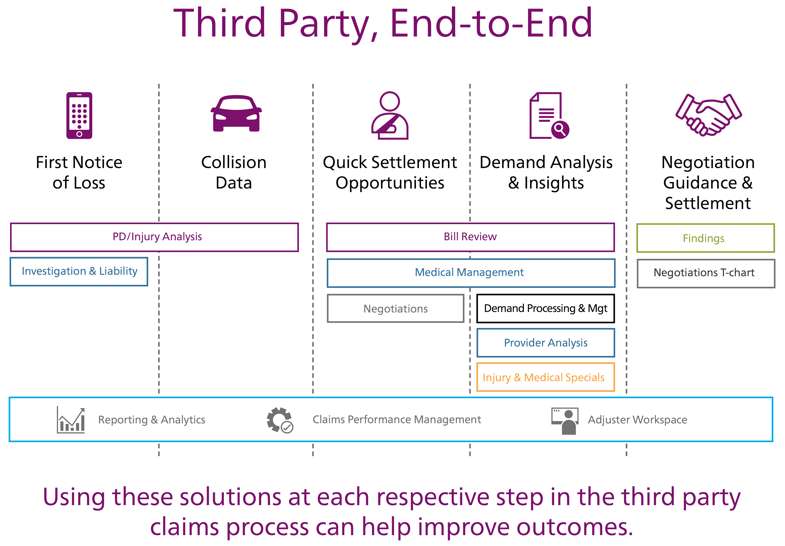

Effectively adjudicating third party auto casualty claims can be a complex web of analysis and decision-making that challenges even the most experienced adjusters. Each of the many decisions made during the lifecycle of a third party claim can potentially affect the outcome—for better or for worse. To avoid claims spiraling out of control, sky-high medical costs, lengthy claim open times and drawn-out negotiations with claimant attorneys, it is important that every person handling the claim make data-driven decisions every step of the way to improve outcomes for the insurer and the claimant. The ideal arrangement is for an adjuster to work out of an expert workspace that complements the claims management system by providing smarter guidance and simplified integration. This adjuster workspace connects and surfaces all of the key data points throughout the claim, including First Notice of Loss (FNOL), provider, medical review, physical damage and settlement data. At the same time, it is also essential that this experience provide guided insights to the adjuster at key decision points and simply not overwhelm them with information.

Gathering and analyzing the right data at FNOL can help indicate the course of a claim and assist with triage to ensure that carriers are handling the claim efficiently.

Consider Data from the Full Claims Lifecycle

Within their workspace, an adjuster should have access to an evolving picture of the claim as it develops comprised of key data from FNOL, vehicle damage estimates, details on treating providers, and medical billing and treatment analysis. By viewing the claim holistically and seeing how all of the data points t together, an adjuster is more prepared to make the best decisions.

FNOL

Gathering and analyzing the right data at FNOL can help indicate the course of a claim and assist with triage to ensure that carriers are handling the claim efficiently. For example, depending on the likelihood that injuries and associated medical treatments will be reported, carriers can make more intelligent assignment decisions and avoid having to transfer the claim during the process. Early data and analytics can help managers prioritize claims by probable severity, helping improve efficiency and giving adjusters the opportunity to focus on claims where they can make the most impact early on.

Vehicle Damage Data

Adjusters can use physical damage data to help assess the potential severity and relatedness of injuries to the accident potentially helping insurance companies improve outcomes. By having access and an integrated analysis of damage data, adjusters can get a better picture of the overall claim. It can help signal early-on how long it might take to close the claim based on severity or in cases where medical treatments might be unusual based on the specifics of the vehicle damage. In addition, physical damage analysis can be a key piece for adjusters in attorney negotiations on third party claims. By understanding the severity of the accident based on this data, adjusters are able to negotiate treatment costs based on the potential relatedness of the injuries to the accident.

Another area where data may come into play in the future is information coming from smartphones, in-vehicle sensors and telematics systems. As these systems become more widely deployed in vehicles, this information could play a role in FNOL notification and provide additional information on accident dynamics.

Provider Analytics

Understanding the dynamics of the medical providers associated with a claim is another way to help adjusters get a better picture of the full claim as part of an end-to-end third party solution. An in-depth database of provider history across industries can help an adjuster see, for example, if a certain provider treats patients differently depending on claim type, like health, auto or workers’ compensation. Tracking provider history can also help insurance companies fight fraud, waste, and abuse by flagging involvement of potential “bad actors” for further scrutiny and helping realize potential linkages between providers and attorneys. By having more insight into provider activity and patterns, insurers can also focus in on preventing soft fraud by benchmarking a provider’s treatment patterns and charges against their peers to help steer some build-up claims to a better result.

Medical Analysis

Medical data from a claim—especially a claim with attorney representation—can be complicated, but provides necessary insight into the claim. To analyze medical and billing data properly, adjusters need a few key tools, including nurse review services and a bill review solution. Key data and information from these sources should surface in an adjuster’s workspace to help them get a full picture of treatment length, injury relatedness and severity, and identify potential bad treatment patterns. The adjuster should be able to go into their workspace and understand how these data points t into the big picture of the claim and be able to drill down to the level of detail they need for each piece. This way, the adjuster can enter attorney negotiations with simplified recommendations and guidance on explaining complex issues.

Data-Driven Decisions

By incorporating a variety of data and insightful guidance in their workspace, an adjuster is more prepared to make thoughtful, data-driven, defensible decisions throughout each stage of a third party claim. By recognizing the value of looking at the claim holistically throughout the claims lifecycle and using data and analytics to help every step of the way, insurance companies can start to improve customer outcomes, ultimately paving a better path to quickly restoring people’s lives.